The purpose of this post is to identify which investors are most active in Social Business, and segment them from early to late stage funding.

I frequently provide due diligence calls to VCs, and also advise startups on their growth startup in highly saturated growth markets. To hone my industry interactions, I’m publishing data on my continued research on funding in the Social Business space (read other posts on the state of funding in social business, and rate of material event or click the VC category to see all posts). The investors are a key factor in the success of a startup, they advise, provide resources for rapid growth, influence a sale or IPO, or can cause a startup to be stymied by innovation through interfering with the executive team. To best understand how investors have influenced the Social Business Software space, we’ve conducted analysis to derive patterns of investors.

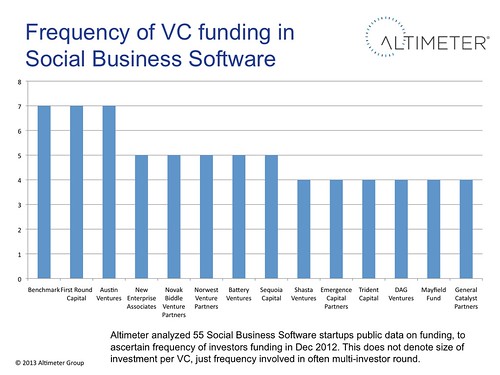

[Austin Ventures, Benchmark, and First Round Capital lead the Social Business Software Funding in Frequency of Investments]

Summary

Funding in the Social Business Software space spurred market traction over the last 5 years, often creating a set of clones with limited feature differentiation. Across all stage investments, Austin Ventures showed dominance in frequency of investing in funds, although their total amount of funding is not public record. As expected, there was a plethora of Angel Investors as companies were just getting out of the garage (sub $1m investment). In early stage funds ($1-5M), Austin Ventures, First Round, Floodgate, were the most active. In mid-stage ($5-10m) Battery and First Round showed increased frequency over other investors, in late-stage ($10-20m), Benchmark Capital was frequently involved, and at mature stage (over $20m), Bay Partners and Institutional Ventures were most frequently involved. Entrepreneurs should use these tables to identify ideal investors per startup maturity to reduce time in seeking institutional funding.

Scope and Method of Research

- Definition of Social Business Software: SaaS based software companies that provide social software to corporations to use. Popular names include Jive, Buddy Media, Radian6, Lithium, Hootsuite. This does not include consumer social networks like Facebook and Twitter, a report I’ll publish in near future.

- Definition of VC, Investor, Angel: These are all investors in the Social Business Software spaces. They often receive money from LPs (Limited Partners) who charge them for investing in markets. On average, VC firms have a 1-3% management fee of overall fund they manage, and have a carry of 10-30% of total take of return from a fund.

- Altimeter conducted analysis of a data set of 55 Social Business Software companies (see list here) in Dec, and has not updated data set to reflect recent funding events, including Sprinklr, Spredfast this week.

- One caveat that applies to all the following data, we cannot determine specific amount of which VC firm or investor has put into each round of investment. Even within the financial S-1 docs there’s cloudy wording on which firm put in what amount.

The following VC firms have invested in the most rounds of Social Business Software vendors, as stated in above caveat, this does include total amount invested, only frequency. Austin, Benchmark and First Round have invested the most frequently, across all stages of funding.

| VC Firm | Total Rounds Involved In |

| Austin Ventures | 7 |

| Benchmark | 7 |

| First Round Capital | 7 |

| Battery Ventures | 5 |

| New Enterprise Associates | 5 |

| Norwest Venture Partners | 5 |

| Novak Biddle Venture Partners | 5 |

| Sequoia Capital | 5 |

| DAG Ventures | 4 |

| Emergence Capital Partners | 4 |

| General Catalyst Partners | 4 |

| Mayfield Fund | 4 |

| Shasta Ventures | 4 |

| Trident Capital | 4 |

(Figure 2) Angel Investors: VCs that invested in rounds under $1M in Social Business Software

We found 18 investors that invested in Social Business Software cateogry under 1 million, while many are individual angel investors, there are a few firms involved, and even Facebook’s fund which invested in early startups to grow the application platform. I often have observed that some of these CEOs have self-invested in their own companies. These investors often provide key advice to helping entrepreneurs launch their company. None of them invested more than once in under a 1 milion round, per public records.

| VC Firm or Individual | Rounds involved in under $1M |

| Colin Evans | 1 |

| Diego Canoso | 1 |

| Eden Ventures | 1 |

| fbFund | 1 |

| ff Venture Capital | 1 |

| Hillsven Capital | 1 |

| Joe Lonsdale | 1 |

| John Levinson | 1 |

| Joshua Stylman | 1 |

| Lightbank | 1 |

| Mayynard Webb | 1 |

| Paige Craig | 1 |

| Peter Hershberg | 1 |

| Seedcamp | 1 |

| Shane Spitzer | 1 |

| Travis Kalanick | 1 |

| Vince Broady | 1 |

| Zelkova Ventures | 1 |

(Figure 3) Early Stage Investors: VCs that invested multiple times in $1-5m rounds in Social Business Software

| VC Firm | Rounds involved in $1M – $5M |

| Austin Ventures | 4 |

| First Round Capital | 3 |

| Floodgate | 3 |

| Adobe Ventures | 2 |

| Anthem Venture Partners | 2 |

| Battery Ventures | 2 |

| BDC Venture Capital | 2 |

| Brightspark Ventures | 2 |

| DFJ Esprit | 2 |

| DFJ Frontier | 2 |

| General Catalyst Partners | 2 |

| Granite Ventures | 2 |

| Metamorphic Ventures | 2 |

| Novak Biddle Venture Partners | 2 |

| RPM Ventures | 2 |

| Summerhill Venture Partners | 2 |

| TEF3 | 2 |

(Figure 4) Mid-Stage Betters: VCs that invested multiple times in $5-10m rounds in Social Business Software

| VC Firm | Rounds involved in $5M – $10M |

| Battery Ventures | 3 |

| First Round Capital | 3 |

| Austin Ventures | 2 |

| Benchmark | 2 |

| Constantin Partners | 2 |

| Mayfield Fund | 2 |

| Norwest Venture Partners | 2 |

| Redpoint Ventures | 2 |

| Shasta Ventures | 2 |

| Trident Capital | 2 |

(Figure 5) Late Stage Investors: VCs that invested in $10-20m rounds in Social Business Software

| VC Firm or Individual | Rounds involved in $10M – $20M |

| Benchmark | 4 |

| DAG Ventures | 3 |

| Emergence Capital Partners | 3 |

| New Enterprise Associates | 3 |

| Sequoia Capital | 3 |

| Mayfield Fund | 2 |

| Novak Biddle Venture Partners | 2 |

| Scale Venture Partners | 2 |

| Shasta Ventures | 2 |

| Advance Publication | 1 |

| Advent Venture Partners | 1 |

| Austin Ventures | 1 |

| Credit Suisse | 1 |

| Dace Ventures | 1 |

| El Dorado | 1 |

| First Round Capital | 1 |

| FTV Capital | 1 |

| General Catalyst Partners | 1 |

| Institutional Ventures | 1 |

| Intel Capital | 1 |

| InterWest Partners | 1 |

| JK&B Capital | 1 |

| Nigel Morris | 1 |

| Norwest Venture Partners | 1 |

| OMERS Ventures | 1 |

| Ron Conway | 1 |

| Steve Case | 1 |

| Sutter Hill Ventures | 1 |

| Ted Leonsis | 1 |

| Tenaya Capital | 1 |

| Trinity | 1 |

(Figure 6) Mature Stage Investors : VCs that invested in rounds over $20m in Social Business Software

| VC Firm | Rounds involved in $20+M |

| Bay Partners | 2 |

| Institutional Ventures | 2 |

| ABS Capital Partners | 1 |

| El Dorado | 1 |

| GGV Capital | 1 |

| Greycroft Partners | 1 |

| Insight Ventures | 1 |

| InterWest Partners | 1 |

| Kleiner Perkins Caufield & Byers | 1 |

| Michael Scissons | 1 |

| New Enterprise Associates | 1 |

| Norwest Venture Partners | 1 |

| SAP Ventures | 1 |

| Sequoia Capital | 1 |

| SoftBank Capital | 1 |

| Syncapse | 1 |

| Trident Capital | 1 |

| Trinity | 1 |

| Val Katayev | 1 |

Conclusion

While not all startups took funding, the venture community is a key component of the social business software category, accelerating growth, jobs, and innovation. Startups should identify which VCs are best fits for their investment strategy, based on maturity and needs. Most VCs are segmented by different stages of investing, with different value propositions to startups beyond money. Buyers who’re purchasing social business software should understand the deeper relationship of investors and the startups in which they’re purchasing.

Comments are closed.